Is the EU's single market and Eurozone even good for economic growth?

I ran 1000s of regression models to find out.

Since I can remember I’ve been told that prominent economists say that the European Single Market (tariff free zone) is good for business and the economy at large. And the Eurozone plausibly eases the difficulties of doing business since there was no need for currency conversions and losses. Thus, we would expect there to be robust and obvious evidence of these claims if we check the data. Now, one could check the various published economist studies, and one would have to try sorting between all their p-hacked results and deal with the murky question of pro-EU bias in general. But given how quick AIs are at coding, we can also just do the research ourselves, so I’ve decided to do that.

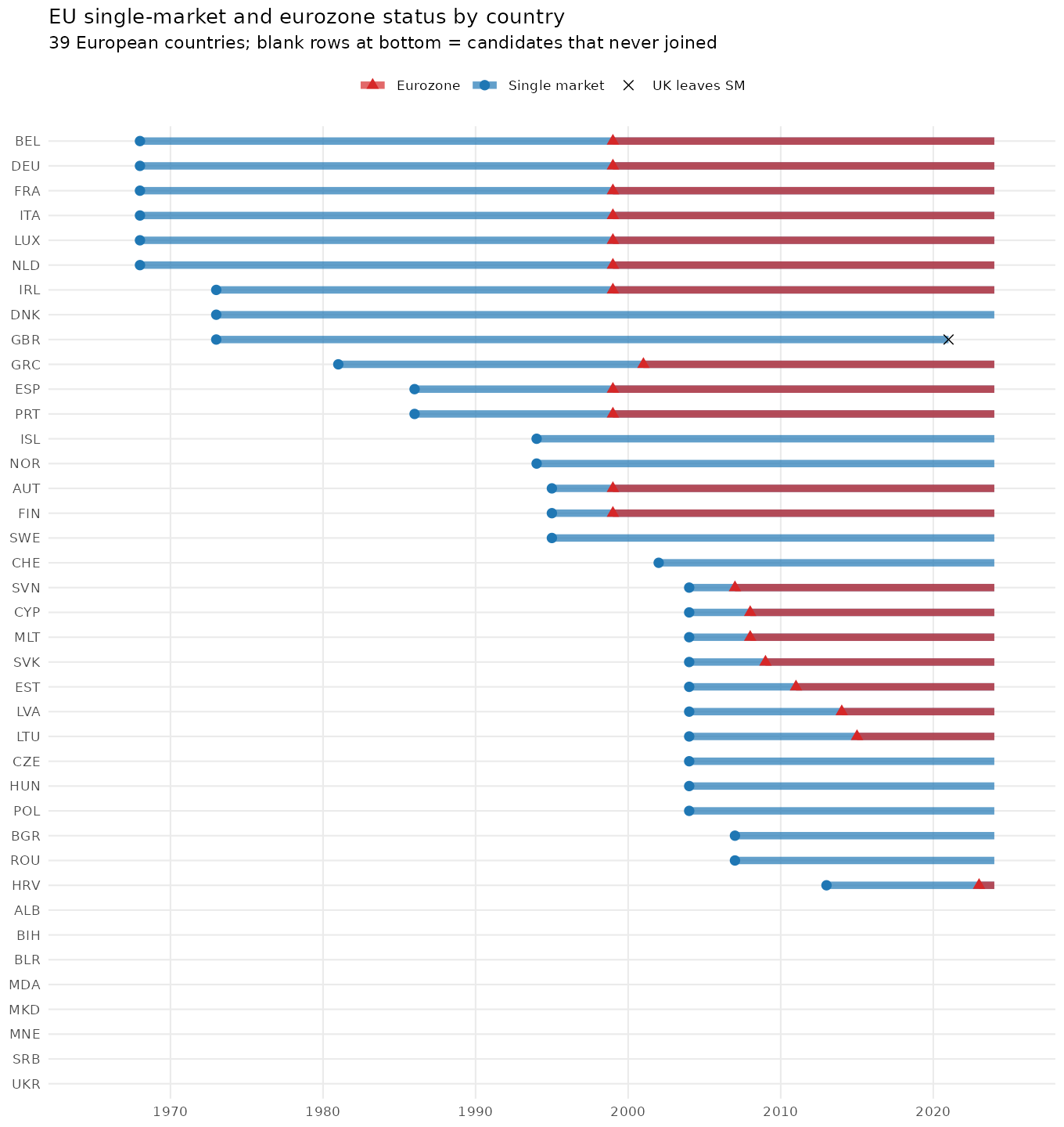

The main analytic leverage for guessing at causality here is that countries changed status for the putative causal variables, and this is easy to measure. That is, the single market started with the European Economic Community in 1957 (Treaty of Rome), the initial customs union (Belgium, France, Italy, Luxembourg, the Netherlands and West Germany). It then gradually expanded over time to include more countries and more internal free trade. Thus, we can use the same country’s data from before and after they entered this union. Similarly, for the Eurozone, we can use the year they joined the Euro and adopted the currency. Thus, we don’t need to worry about between country differences so much because we are using within country variation and with year fixed effects. These are the dates for joining the two systems:

The dataset includes only countries that could plausibly join the European Union, so only European ones, including the ones that so far haven’t joined. These don’t affect the models much since they don’t have any within country variation to use to estimate the main predictor, but are shown here for completion’s sake.

The outcome variable is typically some kind of measure of economic growth. Typically GDP/cap is used, but it has severe issues for the European countries due to the tax haven problems (Ireland) and EU bureaucrats, lobbyists, and employees (Luxembourg), as covered in the prior post on economic growth as function of national IQ and poverty since 2000. The alternatives to GDP/person are GNI/person (foreign workers’ production is counted in their home countries, not their resident countries), and consumption/person (actual spending/person). The GDP/person time series covers more years, but at the cost of being ambiguous. Thus, a typical trade-off between measurement quality and data coverage. My preferred metric, median income, had too few years of coverage to be useful here, which was also true for GNI/person, so we were left with only consumption/person as a more clean metric.

Concerning the data source, for the oldest running time series, we have to use the Maddison database, and for later data we can use PWT‘s. These providers don’t provide the same metrics, so this choice also affects the metric used (GDP/consumption).

A number of other choices presented themselves. For instance, we saw before that being initially poor predicts faster growth, in particular if the IQ is relatively high for the current economic performance. This is a typical catch-up effect, also seen with children who have been out of school for a while. Since we are using fixed effects for countries, any stable characteristic is already controlled for, so there is no need (or possibility) of including the presumed stable NIQs (one could use varying PISA scores but coverage is not great and neither is the meaning of the changes clear). But we can still include a control for current economic performance (for that country x year). I decided to try 3 options: 1) no control, 2) last year’s economic performance, 3) last year’s relative economic performance (1 = average of countries that year).

Since the answers to which combinations of metrics, years, data sources, outlier handling etc. were not obvious, I ran a multiverse/specification curve model with these researcher degrees of freedom:

Data + metric: PWT+GDP, PWT+consumption, Maddison-GDP

Time: full (1950-present), 1991-present

Prior performance: none, lag(econ perf), lag(relative econ perf)

Outliers: none, trimmed

Greece: include, exclude

Estimator: double FE, Sun-Abraham (heterogeneity robust)

Single market coding: accession year, max(accession year, 1993), 1968 (Treaty of Rome in full effect)

Brexit: UK out in 2021, or still in

Croatia: included, excluded (it has only 2 years of data after joining the Eurozone, confounded with post-COVID lockdown recovery)

These choices result in 100s of models for both of the putative causal variables (single market, Eurozone), but fortunately, we can fit all of them quickly: